New section 115BAC is embedded in Income Tax Act by the Finance Act 2020 and it is pertinent w.e.f first April 2020 and will be appropriate on Individuals and HUFs for evaluation year 2021-22 and resulting appraisal years. Under this section taxpayers i.e Individuals and HUFs has an option to pay the tax based on concessional piece rates subject to certain conditions. The new income tax chunk rates according to section 115BAC are as per the following:

Along these lines, it is entirely clear that while the old regime had diverse tax chunks for various age gatherings, new tax doesn’t give the changed tax sections on premise the age gatherings. Conditions to opt new tax plot – In request to profit the advantage of section 115BAC, an individual/HUF assessee needs to renounce the ‘predetermined Exemptions and Deductions’ under different parts and sections of the Income Tax Act which are as per the following: • Leave travel concession as contained in statement (5) of section 10;

House lease stipend as contained in proviso (13A) of section 10; • Some of the recompense as contained in condition (14) of section 10; • Allowances to MPs/MLAs as contained in statement (17) of section 10; • Allowance for income of minor as contained in proviso (32) of section 10; • Exemption for SEZ unit contained in section 10AA; • Standard reasoning, derivation for diversion remittance and business/proficient tax as contained in section 16; • Interest under section 24 in regard of self-involved or empty property alluded to in sub-section (2) of section 23. (Misfortune under the head income from house property for leased house will not be permitted to be set off under some other head and would be permitted to be conveyed forward according to surviving law); • Additional censure under proviso (iia) of sub-section (1) of section 32; • Deductions under section 32AD, 33AB, 33ABA; • Various reasoning for gift for or use on logical research contained in sub-statement (ii) or sub-condition (iia) or sub-condition (iii) of sub-section (1) or sub-section (2AA) of section 35; • Deduction under section 35AD or section 35CCC; • Deduction from family benefits under provision (iia) of section 57; • Any conclusion under part VIA (like section 80C, 80CCC, 80CCD, 80D, 80DD, 80DDB, 80E, 80EE, 80EEA, 80EEB, 80G, 80GG, 80GGA, 80GGC, 80IA, 80-IAB, 80-IAC, 80-IB, 80-IBA, and so on).

Download Automated Income Tax Master of Revised Form 16 Part B for the Financial Year 2019-20 [ This Excel Utility can prepare at a time 50 employees Form 16 Part B in Excel]

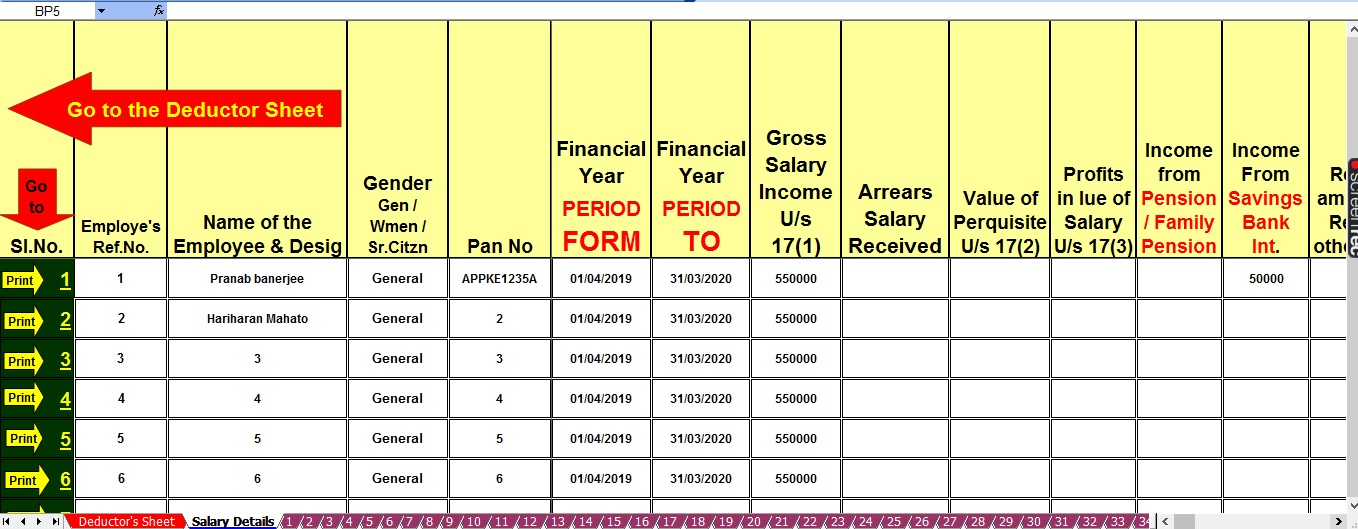

Be that as it may, conclusion under sub-section (2) of section 80CCD (business commitment because of worker in advised annuity plan) and section 80JJAA (for new work) can be guaranteed. Models for Comparative examination of Old Vs New Tax regime: – Assume 60 years old enough gathering – Deductions Applicable: Rs 1.5 Lakh u/s 80C; Rs. 50,000 standard derivation; Rs. 25,000 u/s 80D; Rs. 2 Lakh home advance intrigue u/s 24. Aggregate of Rs 425000/ – Total Tax Calculated is including Tax+ Edu Cess (Surcharge isn’t Calculated)

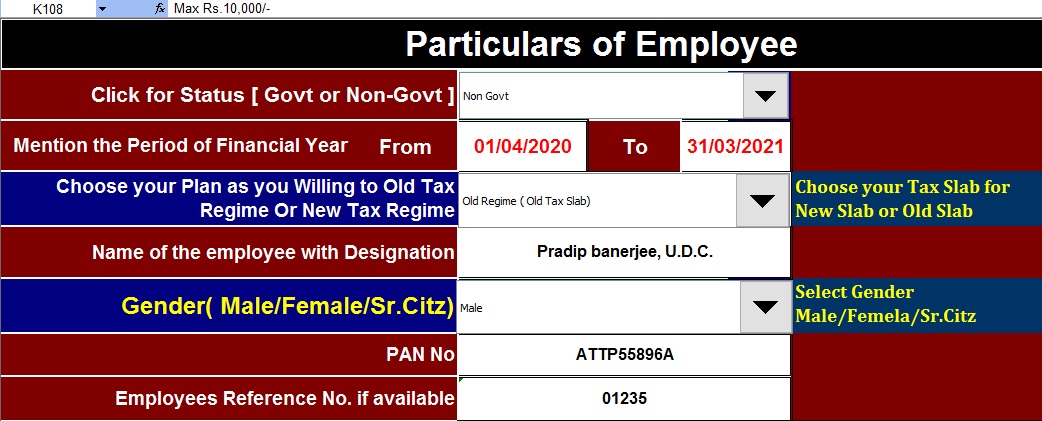

Choice of New or Old Tax Regime relies on certain components which are clarified as follows: 1. Nature of Income: Whether assesse’ s of Income is just from the “Pay” or it will incorporate income from different heads later in the current monetary year i.e between 01.04.2020 to 31.03.2021. On the off chance that assessee is expecting his income from different heads for which sum can’ t be resolved in the start of budgetary year or whenever before the finish of applicable money related year then assessee ought not make rush to opting the tax regime old or For instance commonly a salaried representative get a few incomes from his boss in the mid or before monetary year’s over like Bonus, Performance related compensation and so forth for which worker wear’ t know the specific sum which is required to be gotten in the mid or before the finish of pertinent monetary year. So income is a variable factor while opting old or new Tax Regime and must be considered and appropriately examined by the assessee. 2. Exceptions/Deductions to be benefited: Before opting the old or new Tax Regime assessee must audit all the exclusions/deductions which are to be profited by him like number of exclusions/deductions, quantum/measure of exceptions/deductions and their effect on taxable income i.e whether is there any adjustment in chunk of his income such because of exclusions/deductions. For instance now and then assessee has less number of exclusions/deductions with exceptionally low effect on taxable income like an assessee could conceivably have enthusiasm on lodging advance which is accessible for conclusion U/S 24(b) of Income Tax Act 1961 or if assessee has the equivalent however sum isn’t as much as it will change the section of Income subsequent to thinking about the equivalent. Henceforth it is counsel to all the taxpayers covers u/s 115BAC that make legitimate investigation of your Tax risk before opting old or new Tax Regime, even this section additionally given that assessee can opt old or new Tax Regime before recording his arrival of income. So it is encouraged to all taxpayers that they ought to opt the old or new Tax Regime just while record your income tax return. Note: To ascertain/get to your tax risk under both old and new Tax Regime you may allude income tax number cruncher F.Y 2020-21 which is accessible at incometaxindiaefiling.gov.in https://www.incometaxindiaefiling.gov.in/Tax_Calculator/index.html?lang=eng What are the conditions to benefit the new regime and who can opt it? 1) Any Individual can opt the new tax regime, which means to state that the new regime is an optional regime and Individual taxpayers can pick between the old and new tax regime. 2) Further, where the taxpayer acquiring income from business has opted for the new regime for any year and pulls back it in any resulting year, can’t opt for the new regime again and needs to follow the old tax pieces as it were. Notwithstanding, other Individual taxpayers can pick between the regimes consistently. 3) CBDT roundabout gave on April 13, 2020 has guided all the businesses to get an announcement from representatives, on the off chance that they wish to opt for the new tax regime. Be that as it may, representatives will at present keep on reserving the option to pick between the tax regimes at the hour of documenting the arrival. People opting for the new regime needs to forego certain exceptions and deductions which were accessible with the old regime. CBDT has given a roundabout C1 of 2020 dated thirteenth April on explanation of TDS under section 115BAC . Primary concerns which are explained by CBDT through this roundabout are as per the following: 1. On the off chance that a representative having Income from other than Income under the head “Benefits and Gains of Business or Profession” and ready to opt new Tax Regime U/S 115BAC may hint the duductor being his manager of such goal on each monetary year and upon such implication the deductor will process his absolute income and deduct TDS appropriately. In the event that such suggestion isn’t made by representative the business will make TDS without thinking about the arrangements of section 115BAC. 2. It is likewise explained that if implication made by worker to opt new Tax Regime U/S 115 BAC and ready to deduct TDS in like manner during the monetary year in such case the representative can’t alter his option during money related year to opt old Tax Regime. Anyway at the hour of documenting of return of income the option could be not quite the same as the insinuation that made by such representative to the business for that money related year.

Feature of this Excel Utility:-

1) This Excel Utility prepare as per Budget 2020 and this Utility can calculate Old and New Tax Regime as per New section 115BAC

2) This Excel Utility can use both of Govt and Non-Govt Employees

3) The Salary Structure is made as per the all Govt and Non-Govt Employees as per the Govt and Non-Govt concern’s Salary Pattern.

4) Automated House Rent Exemption Calculation U/s 10(13A)

5) Automated Salary Arrears Relief Calculation U/s 89(1) with Form 10E from the F.Y. 2000-01 to F.Y. 2020-21 ( Updated Version)

6) Automated Revised Form 16 Part A&B ( Who are not able to download Form 16 Part A, they can use this Part A&B)

7) Automated Revised Form 16 Part B

Leave a Reply