Did you receive any advance salary or arrears of salary? If yes, you might be worried about the tax implications of the same. Do I have to pay taxes on the total amount? What about the tax calculations of the previous year and so on? Taxpayers who have such questions in their mind, here is all that you need to know.

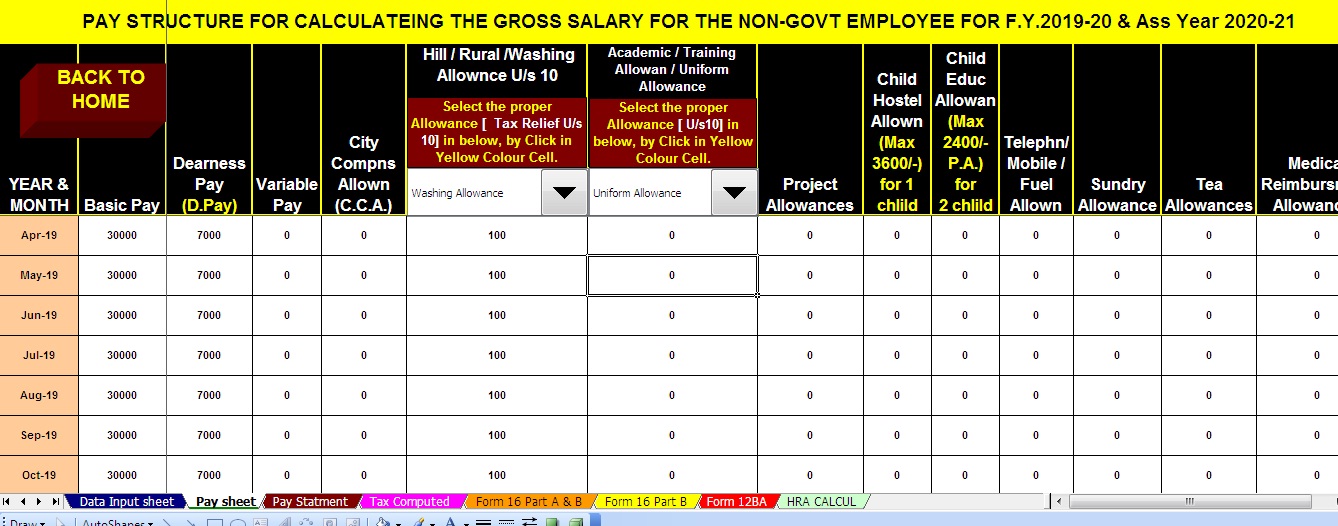

Download Automated Income Tax House Rent Exemption Calculator U/s 10(13A) in Excel Format

By now, you would have already figured out that income tax is calculated on the total income of a taxpayer for a certain year. The income can either be in the form of salary or family pension or other sources of income. However, there might be scenarios where you have received arrears of family pension or pending salary during the current fiscal year. It can happen that an income tax payer gets a part of his profit or salary in advance or as arrears in any financial year, which increases his total income thereby increase the payable taxes. In such a case, an application can be made and the assessing officer can grant a relief to the tax payer. To sum it up, the Income Tax Act ensures there is parity in the income tax slab rates, and thus, when a portion of the income received does not pertain to the current year, a relief is granted so that the taxable income does not increase.

Download Automatic Income Tax Preparation Excel Based Software for only Private Employees For Financial Year 2019-20

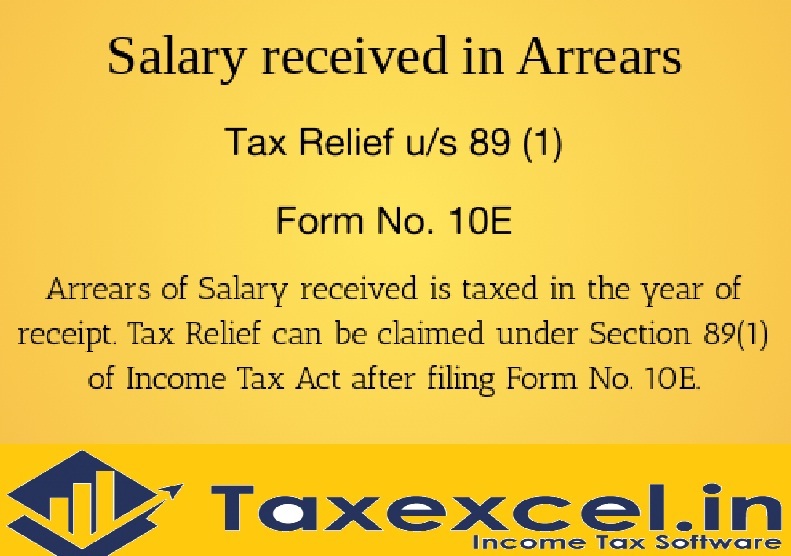

To ensure that you are not burdened with paying additional taxes, the income tax department provides Relief U/s 89(1). If you receive any pension or payments for the previous year, you will not be taxed on the total amount for the current year. Essentially keeping you away from paying extra taxes, because there was a delay in payment.

To avail the benefits under Section 89(1) you would need to submit Form 10E. What is Form 10E would be the most obvious question. The details of Form 10E, along with how and why to submit the same is provided in detail below.

What is relief under section 89(1)?

When the taxpayer receives:

- Arrears of salary or

- Advance salary or

- Arrears of family pension

then such amount is taxable in the Financial Year in which it is received.

However, relief under section 89(1) is provided to reduce additional tax

Burden due to delay in receiving such income.

How to calculate relief under section 89(1)?

Here are the steps to calculate relief under section 89(1) of Income Tax Act, 1961:

- Calculate tax payable on total income including arrears in the year in which it is received.

- Calculate tax payable on total income excluding arrears in the year in which it is received.

- Calculate difference between (1) and (2).

- Calculate tax payable on total income of the year to which arrears are related, including arrears.

- Calculate tax payable on total income of the year to which arrears are related, excluding arrears.

- Calculate difference between (4) and (5).

- The amount of relief will be the excess amount of (3) over (6). No relief shall be allowed if the amount of (6) is more than the amount in (3).

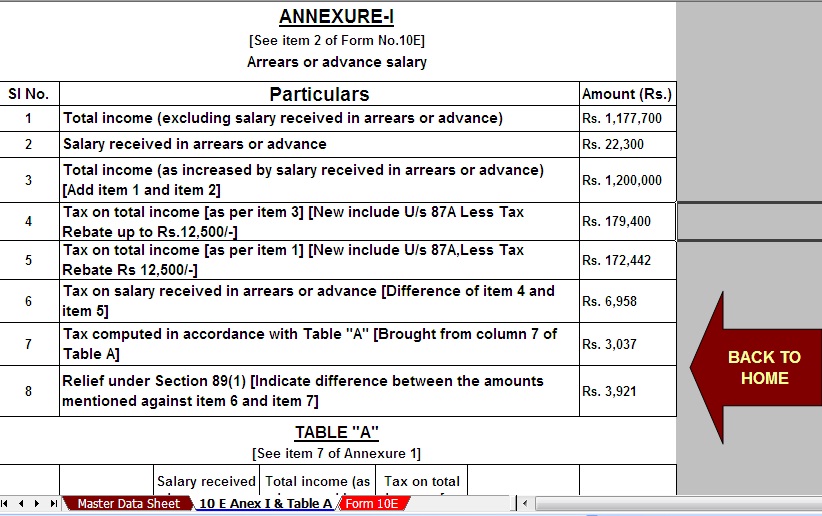

Example on how to calculate relief under section 89(1)

Mr. A has total income of Rs. 6,00,000/- for Financial Year 2017-18 (Assessment Year 2018-19) and received arrears of Rs. 1,50,000/- for Financial Year 2011-12 (Assessment Year 2012-13). The total income for Financial Year 2011-12 is Rs. 2,00,000/-.

The relief will be calculated as follows:

- Tax on total income of Rs. 7,50,000/- (Rs. 6,00,000+Rs. 1,50,000) including arrears for F.Y. 2017-18 is Rs. 64,375/- (as per rates applicable for F.Y. 2017-18 i.e. A.Y. 2018-19).

- Tax on total income of Rs. 6,00,000/- excluding arrears for F.Y. 2016-17 is Rs. 33,475/-

- Difference between (1) and (2) is Rs. 30,900/- (as per rates applicable for F.Y. 2017-18 i.e. A.Y. 2018-19).

- Tax on total income of Rs. 3,50,000/- (Rs. 2,00,000+Rs. 1,50,000) including arrears for F.Y. 2011-12 is Rs. 17,510/- (as per rates applicable for F.Y. 2011-12 i.e A.Y. 2012-13).

- Tax on total income of Rs. 2,00,000/- excluding arrears for F.Y. 2011-12 is Rs. 2,060/- (as per rates applicable for F.Y. 2011-12 i.e A.Y. 2012-13).

- Difference between (4) and (5) is 15,450/-

- The amount of relief will be Rs. 15,450/- [excess amount of (3) over (6)]

What is Form 10E?

For claiming relief under section 89(1) for arrears of salary received, it is mandatory to file Form 10E with the Income Tax department. If Form 10E is not filed and relief is claimed, then the taxpayer is most likely to receive notice from Income Tax department for not filing Form 10E.

Leave a Reply