The Section 80D contains grants a tax deduction on medical insurance charges and medical use. It is granted on the expenses paid for a medical insurance strategy for the taxpayer himself and/or a nearby family member. Section 80D of Income Tax offers a deduction over and above to the deductions under Section 80C of Income Tax Act

Deduction under Section 80D

• The maximum permissible deduction is INR 25,000 each financial year on the charge for health insurance for self and family.

• For senior residents, the maximum permissible deduction is INR 50,000 for every financial year.

Download Automated Income Tax Arrears Relief Calculator U/s 89(1) For the Financial Year 2020-21

Qualification under Section 80D

An occupant individual can avail the deduction, according to section 80D, against the top notch paid for health insurance administrations for below family members

• Self

• Children

• Spouse

Any inhabitant individual or HUF is qualified for a tax deduction on the use incurred towards the maintenance of ward disabled relative under Section 80DD of the Income Tax Act, 1961. This deduction cannot be availed by a taxpayer who is oneself disabled. The deduction is available for below-referenced costs:

(a) Consumption incurred towards medical treatment, training, nursing and rehabilitation of a disabled ward relative.

(b) Amount paid towards a plan of LIC/UTI another regulated insurer for maintenance of disabled ward relative.

For the inclusion of ward disabled relative, here are the important terms and conditions

Download Auto Calculate Income Tax Software in Excel All in One for the Govt & Non-Govt Employees for the F.Y.2020-21 along with Form 10E

Disabled Individual

• In cases for the individual taxpayer: mate, youngsters, parents, brothers and sisters of the individual, or any of them who is mainly or completely subject to such individual

• In the case of HUF: Any member of the HUF, who is mainly or entirely reliant on such HUF. Subject to the condition that the needy individual has not claimed any deduction under section 80U.

Disability

The cases where an individual is suffering from disability include low vision condition, blindness, sickness restored, loco motor’s disability, hearing impairment and any kind of mental disease or mental retardation including autism.

An individual with an extreme disability means:-

The cases where an individual with extreme disabled (80%) because of single or different disabilities including the cases of autism, cerebral palsy and mental retardation.

Download Auto Calculate Income Tax Software in Excel All in One for the Non-Govt(Private) Employees for the F.Y.2020-21along with Form 12BA

Permissible Cutoff points

The maximum permissible deduction under this section is up to INR 75,000 towards the consumption incurred in the maintenance of ward disabled relative, independent of its amount. In cases of extreme disability i.e., disability of 80% or above, then the amount of deduction will be INR 1,25,000.

Under Section 80DDB of the Income Tax Act, an individual can claim a deduction on the consumption incurred on medical treatment of genuine sicknesses. The provisions in this regard are as per the following:

• You must be an inhabitant individual or a HUF

• The deduction is applicable on the actual amount paid by the individual/HUF on medical treatment of a predetermined disease, as prescribed by the Board.

• In cases of the individual taxpayer, the above-referenced use ought to be on medical treatment of an individual or completely/mainly needy, kids, mate, parents or siblings of the individual.

• In the case of a HUF, the use ought to be for the treatment of any family member, who is entirely/mainly subject to HUF.

• The taxpayer is needed to obtain the recommendation for the predefined medical treatment from any perceived oncologist, neurologist, urologist, immunologist, hematologist or any other specialist, as may be prescribed.

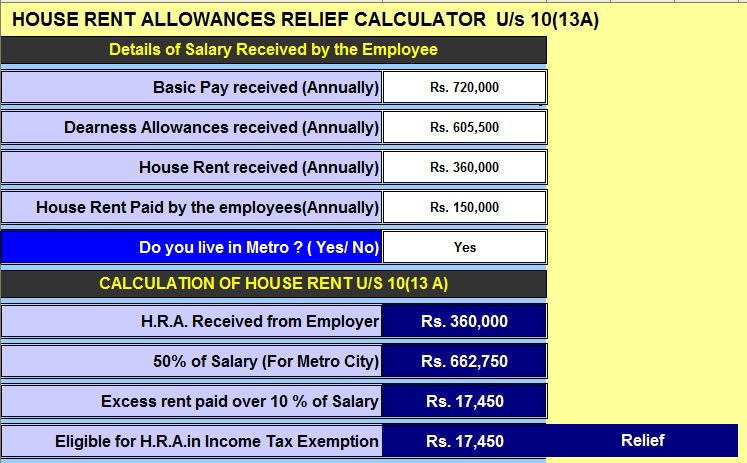

Download Auto Calculate Income Tax Exemption from House Rent Calculator U/s 10(13A)

Diseases secured under Section 80DDB

The nature of diseases and ailments which are included for deduction under Section 80DDB is referenced in Rule 11DD of Income Tax and the same are as per the following:

1. Neuro Diseases as recognized by a Doctor, where the maser of disability has been affirmed to be of 40% and above and covers Dementia, Dystonia Musculorum Deformans, Chorea, Motor Neuron Disease, Ataxia, Aphasia, Parkinson’s Disease and Hemiballismus.

1. Malignant Cancer

2. AIDS-Acquired Immuno-Inadequacy Disorder

3. Chronic Renal failure

4. Haematological disorders like Hemophilia or Thalassaemia.

Amount of deduction

Amount actually paid for the medical treatment indicated above or Rs 40,000 whichever is lower. For senior residents (aged 60 and above) the deduction would be the use incurred or Rs 100,000, whichever is lower.

Key Terms and Conditions for availing Section 80DDB Tax Benefits

• Below referenced are scarcely any critical points to be followed while availing the deduction under section 80DDB:

1. The taxpayer needs to obtain a duplicate of the certificate in Form No. 10-I, appropriately issued and attested by a neurologist/urologist/oncologist/hematologist/immunologist or any such specialist

• The specialist ought to be working in an Administration perceived hospital.

• In case the taxpayer is receiving repayment for such use from any other insurer or his boss, the net amount shall be deducted from the total amount of tax exception processed in an aforesaid manner.

• The taxpayer ought to obtain a duplicate of the certificate issued by the medical authority. A new certificate is mandatory post-reassessment of disability after the expiry time frame referenced in the initial certificate.

• If the ward predeceases, the taxpayer or the member of HUF alluded to above, then the amount paid or stored, shall be charged to tax in the hands of the taxpayer for the earlier year in which such whole is gotten.

• The certificate can be obtained from a specialist doctor according to the cases applicable. In case the patients are being treated in any private hospital, the certificate from the administration hospital is not mandatory.

• The specialist ought to be a post-graduate in General or Internal Medicine or an equivalent degree perceived by the Medical Chamber of India.

Free Download Auto Calculate Income Tax All in One Value of Perquisite U/s 17(1)