NPS has two Tiers – 1 and 2.

NPS Tier 1 is the long haul speculation, which has limited withdrawals and implied essentially for retirement arranging. On development, you can pull back limit of 60% of corpus as lump sum and rest must be utilized for annuity buy.

NPS Tier 2 is for overseeing short to medium term venture. You can contribute and pull back whenever according to your desire. This is a discretionary element and you are inquired as to whether you need Tier 2 record while opening NPS.

All the tax benefits identified with NPS is accessible to interest in NPS Tier 1 record as it were.

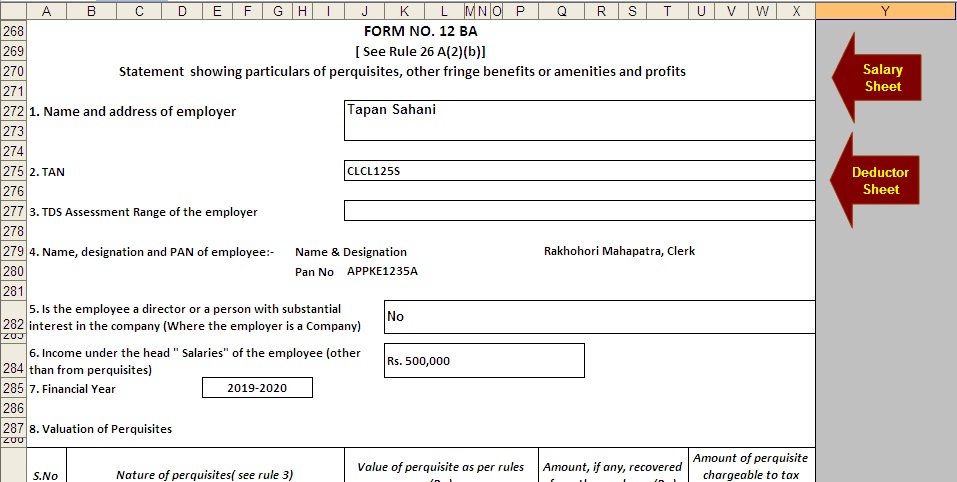

Download And Prepare At a Time 50 Employees Automated Income Tax Form 16 Part B With Form 12 BA (Modified Format) [This Excel Utility Prepare At a time 50 Employees Form 16 Part B With 12 BA in New Format for A.Y. 2020-21]

The main feature of this Excel Utility:-

- Prepare At time 50 Employees Excel Based Form 16 Part B with Form 12 BA ( Modified Format of Form 16 Part B Vide CBDT Notification No.36/2019 Dated 12/04/2019 ]

- All the Amended Income Tax Section have in this utility as per Budget 2019

- You can print individual Form 16 Part B with Form 12 BA

- Most easy to install just like an Excel File

- Easy to Fill the all column

- Automatic Convert the Amount to the In-Words

NPS Tax Benefits:

NPS tax reductions are accessible through 3 Section – 80CCD(1), 80CCD(2) and 80CCD(1B). We talk about each underneath:

1. Section 80CCD(1)

Worker commitment up to 10% of essential pay and dearness stipend (DA) up to 1.5 lakh is qualified for charge derivation. [This commitment alongside Sec 80C has 1.5 Lakh speculation limit for charge deduction]. Independently employed can likewise guarantee this tax break. Anyway the point of confinement is 10% of their yearly pay up to limit of Rs 1.5 Lakhs.

2. Section 80CCD(1B)

Extra exception up to Rs 50,000 in NPS is qualified for annual assessment derivation. This was presented in Budget 2015.

3. Section 80CCD(2)

Boss’ commitment up to 10% of essential in addition to DA is qualified for finding under this area over the Rs 1.5 lakh limit in Sec 80CCD(1). This is likewise gainful for boss as it can guarantee tax reduction for its commitment by demonstrating it as cost of doing business in the benefit and misfortune account. Independently employed can’t guarantee this tax reduction.

NPS – Illustration of Tax Exemption on Employer Contribution

Tax reduction for Compulsory NPS reasoning:

The previous benefits structure was supplanted by NPS in generally focal and state government occupations since 2004. So any individual who joined after that has necessary derivation for NPS. The reasoning is 10% of essential compensation and dearness stipend (DA) and the business also contributes the coordinating sum. The disarray for most representatives is how they take tax cut on their mandatory NPS derivation?

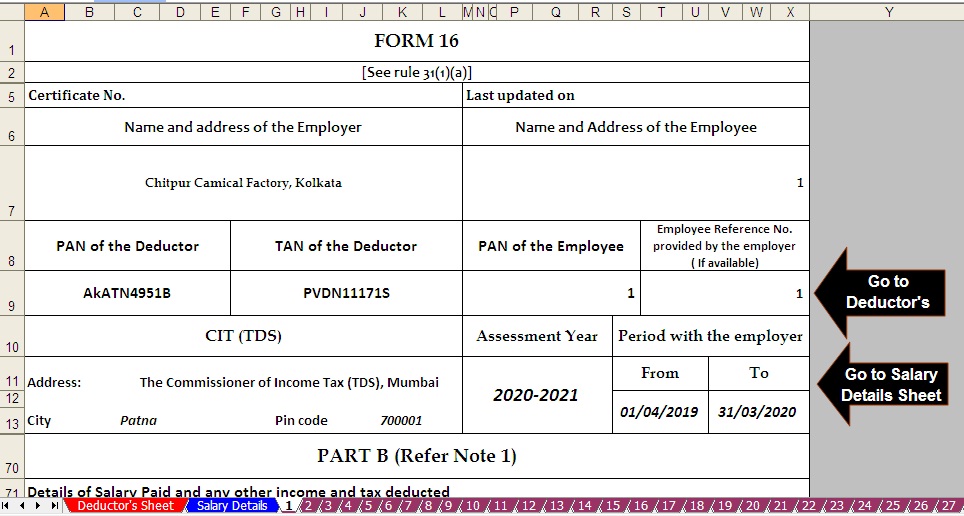

Download And Prepare At a Time 50 Employees Automated Income Tax Form 16 Part B (Modified Format) [This Excel Utility Prepare At atime 50 Employees Form 16 Part B in New Format for A.Y. 2020-21]

The main feature of this Excel Utility:-

- Prepare At time 50 Employees Excel Based Form 16 Part B ( Modified Format of Form 16 Part B Vide CBDT Notification No.36/2019 Dated 12/04/2019 ]

- All the Amended Income Tax Section have in this utility as per Budget 2019

- You can print individual Form 16 Part B Most easy to install just like an Excel File

- Easy to Fill the all column

- Automatic Convert the Amount to the In-Words

How about we take the simple part first.

Representative’s commitment in NPS would be qualified for charge derivation u/s

80CCD(1).

The representative has a decision with respect to which segment [80CCD(1) or 80CCD(1B)] he needs to show his commitment. In a perfect world he should show Rs 50,000 interest in NPS u/s 80CCD(1B). The assessment reasoning on rest Rs 12,000 can be asserted u/s 80CCD(1). The area 80CCD(1) alongside Section 80C has venture limit qualified for charge derivation as Rs 1.5 lakhs. So he should make extra speculation of Rs 1,38,000 in Section 80C to spare most extreme assessment. In everything he can spare Rs 2 lakhs charge u/s 80C and 80CCD(1B).

Leave a Reply